Ⅰ. Introduction

1. Motivation and Background

2. Literature Review and Research Gap

3. Contribution of This Study

4. Hypotheses and Preview of Findings

Ⅱ. Institutional Background and Hypothesis Development

1. China’s UHV Grid: A Quasi-Natural Experiment

2. Hypothesis Development: UHV Projects and Corporate Operational Risk

3. Exploring the Mechanisms

Ⅲ. Data, Variables, and Empirical Strategy

1. Sample and Data Sources

2. Variable Definitions

3. Empirical Strategy

Ⅳ. Empirical Findings and Discussion

1. Parallel Trends Test Validation

2. Main Results: The Average Treatment Effect

Ⅴ. Further Analysis and Robustness Checks

1. Mechanism Analysis

2. Heterogeneity Analysis

3. Robustness Checks

4. Placebo Analysis: High-Speed Rail Projects

Ⅵ. Conclusion

1. Summary of Findings

2. Implications

3. Limitations and Future Research

Ⅰ. Introduction

1. Motivation and Background

The stability and affordability of energy are foundational pillars of modern industrial economies, serving as critical inputs for corporate production and principal determinants of operational stability. Disruptions in energy supply, such as the power restrictions that can negatively impact economic and social development, underscore the profound reliance of firms on a resilient energy infrastructure (Ren et al., 2025). In this context, China’s development of an Ultra-High Voltage (UHV) transmission grid represents a globally significant infrastructure initiative, unparalleled in its scale, technological sophistication, and strategic ambition. The primary impetus for this massive undertaking is to resolve the fundamental geographical imbalance between China’s energy resources which are concentrated in the western and northern regions and its primary load centers, located in the populous and industrialized eastern coastal provinces (Ren et al., 2025).

The scale of this national project is immense. During the “14th Five-Year Plan” period alone, China planned to construct 38 new UHV lines, spanning over 30,000 kilometers with a total investment of approximately 380 billion RMB. By the early 2020s, the operational UHV grid had already achieved a cumulative power transmission capacity exceeding 2.5 trillion kilowatt-hours (Wang et al., 2024). This endeavor is far more than a simple upgrade of the national power grid; it is a cornerstone of China’s national economic strategy. It has been described as a “national weapon” to promote the revolution in energy production and consumption, coordinate sustainable development, and secure the nation’s energy future (Ren et al., 2025).

The strategic discourse surrounding the UHV grid is notably complex and multifaceted. On one hand, it is heralded as a conduit for clean energy, designed to transmit vast quantities of hydropower, wind, and solar power from the resource-rich west to the energy-hungry east, thereby optimizing the national energy structure and facilitating a green transformation (Ren et al., 2025). On the other hand, some empirical evidence suggests that the grid’s construction, by enabling massive inter-regional power transfers often sourced from large-scale coal power bases, has led to an increase in overall carbon emissions, particularly in power-sending regions (Chi et al., 2023). This inherent tension the grid as a facilitator of both green energy and carbon-intensive power creates a complex empirical landscape. The infrastructure itself is largely agnostic to the “color” of the electrons it transmits, but its existence fundamentally alters the operational environment for firms. This study is motivated by the need to understand how corporations navigate the operational consequences of this complex energy transition, where the stability gained from the new infrastructure is intertwined with the dual possibilities of cleaner energy inputs and greater reliance on traditional fossil fuels.

To summarize, the central narrative of this paper is organized around the causal pathway from UHV transmission projects to reduced corporate operational risk, and further to enhanced green innovation and improved financial flexibility. The analyses of heterogeneity and robustness serve as complementary validation, ensuring that the main argument remains focused on the risk-reduction effect. This structure allows readers to clearly follow the logic of “infrastructure → risk → mechanisms,” while treating subgroup and robustness checks as supporting evidence.

2. Literature Review and Research Gap

A growing body of academic literature has begun to examine the multifaceted impacts of China’s UHV projects. Initial research has focused on macroeconomic outcomes, providing evidence that UHV construction promotes county-level economic growth, although these effects may be concentrated in the short term and vary by region (Sun and Min, 2024). Other studies have investigated the grid’s impact on the energy sector itself, documenting a significant shift away from thermal power generation towards renewable energy production and an increase in the share of electricity in end-use consumption (Ren et al., 2025). The environmental consequences have also been a subject of inquiry, with some studies finding that UHV projects can contribute to reductions in local pollution but may increase overall carbon emissions due to the scale of power generation required (Chi et al., 2023; Gao and Zhao, 2025).

More recently, the research lens has shifted to the firm level. These studies have found that UHV projects enhance firms’ total factor energy efficiency, particularly in non-energy-intensive and manufacturing industries (Wang et al., 2024). There is also evidence that the improved energy infrastructure positively contributes to the value chain upgrading and green transformation of manufacturing firms, driven by mechanisms such as improved capacity utilization and technological innovation (Min and Wang, 2025).

Despite this burgeoning literature, a critical research gap remains. While prior work implies a reduction in firm-level risk through a more stable and reliable power supply (Wang et al., 2024), the direct, causal impact of this massive infrastructure shock on a fundamental measure of firm health corporate operational risk has not been systematically investigated. Operational risk, which captures the uncertainty and volatility in a firm’s core business activities and earnings, is a first-order concern for managers, investors, and regulators (Deng et al., 2023). It reflects the potential for losses arising from inadequate or failed internal processes, human error, system failures, or external events, with disruptions to critical inputs like electricity being a prime example of the latter (Moosa, 2007). Understanding how a major public infrastructure investment like the UHV grid affects this dimension of corporate risk is a key unanswered question at the intersection of accounting, finance, and public policy.

3. Contribution of This Study

This paper aims to fill this gap and makes three primary contributions to the literature. First, it provides the first large-sample empirical evidence on the causal effect of UHV infrastructure development on corporate operational risk. By focusing on a direct measure of earnings volatility, it moves beyond intermediate outcomes like energy efficiency to assess a more holistic measure of firm stability. Second, it employs a robust quasi-experimental research design. Leveraging the staggered, province-by-province rollout of UHV projects, this study utilizes a Difference-in-Differences (DID) framework. Crucially, it addresses the recently highlighted econometric challenges of potential bias in staggered settings by employing state-of-the-art estimators, thereby enhancing the causal interpretation of the findings (Callaway and Sant’Anna, 2020; Goodman-Bacon, 2021). Third, it provides a more nuanced understanding of the UHV grid’s impact by exploring key transmission mechanisms, particularly the role of green innovation, and by examining important sources of heterogeneity across firms and regions. This sheds light not only on whether UHV projects affect risk but also how and for whom these effects are most pronounced.

4. Hypotheses and Preview of Findings

The central hypothesis of this study is that the commissioning of UHV transmission lines, by enhancing the stability and reliability of the power supply, reduces the operational risk of firms located in the connected provinces. To test this, a comprehensive panel dataset of Chinese A-share listed companies from 2007 to 2016 is constructed, merging financial data from the CSMAR database with green patent data from the CNRDS database.

The empirical analysis yields several key findings. The results show that the implementation of UHV projects leads to a statistically and economically significant reduction in corporate operational risk, as measured by earnings volatility. This finding is robust to a battery of alternative specifications and robustness checks. Event study analysis confirms that the parallel trends assumption holds, and it reveals that the risk-reducing effect is dynamic, growing in magnitude in the years following the treatment. Further investigation into the mechanisms suggests that the effect is partially mediated by an increase in corporate green innovation, indicating that a more stable energy environment fosters long-term innovative activities. Finally, the heterogeneity analysis reveals that the risk-reduction effect is more pronounced for non-state-owned enterprises (non-SOEs) and for firms located in designated power-receiving regions, highlighting the differential impact of this national infrastructure project across the corporate landscape.

Ⅱ. Institutional Background and Hypothesis Development

1. China’s UHV Grid: A Quasi-Natural Experiment

Ultra-High Voltage (UHV) transmission technology, defined as alternating current (AC) at 1000kV and above and direct current (DC) at ±800kV and above, represents a significant leap over traditional high-voltage systems. Compared to conventional 500kV lines, UHV technology can triple transmission capacity, extend transmission distance by 2.5 times, and reduce line losses by approximately 45% (Ren et al., 2025). This technical superiority makes it uniquely suited to China’s energy geography, enabling the efficient bulk transfer of power over vast distances.

The development of the UHV grid has been a state-led endeavor, primarily driven by China’s two major grid operators, the State Grid Corporation of China (SGCC) and the China Southern Power Grid (CSG). The rollout has not been simultaneous across the country but has occurred in distinct phases or “waves,” guided by national Five-Year Plans and specific energy development strategies (Ren et al., 2025). For instance, SGCC’s plans for 2013-2020 involved achieving specific “vertical and horizontal” AC grids and a set number of DC lines by target years like 2015, 2017, and 2020. This phased, province-by-province implementation, driven by centralized planning rather than firm-level characteristics, creates a compelling quasi-natural experiment. The staggered timing of when different provinces are connected to the UHV grid allows for the use of a Difference-in-Differences (DID) research design to identify the causal impact of the infrastructure on firms located within those provinces.

<Table 1> provides a detailed list of the UHV projects completed within the primary sample period of this study (up to and including 2016). This table is the cornerstone of the empirical design, as it transparently defines the “treatment” event for each province. By clearly delineating which projects became operational in which year and the key provinces they connected, it makes the UHV_it treatment variable in the subsequent analysis fully replicable and allows readers to understand the precise nature of the quasi-natural experiment. This level of detail is crucial for a credible DID analysis, as the validity of the study hinges on the unambiguous identification of treated and control groups over time.

<Table 1>

UHV Transmission Projects Completed in China and Defining the Treatment Group (2009-2016)

2. Hypothesis Development: UHV Projects and Corporate Operational Risk

Operational risk, in a broad sense, refers to the risk of loss or adverse earnings fluctuations resulting from failures in a company’s day-to-day operations. These failures can stem from internal sources (e.g., human error, system breakdowns) or external events (e.g., supply chain disruptions, regulatory changes) (Moosa, 2007). For industrial and manufacturing firms, a particularly potent external risk is the disruption of critical production inputs, chief among them being electricity (Wang et al., 2024). Frequent power restrictions or unexpected outages can halt production lines, spoil materials, delay shipments, and ultimately introduce significant volatility into a firm’s revenues and costs (Wang et al., 2024).

The commissioning of a UHV transmission line is hypothesized to mitigate this source of risk through a clear causal chain. First, the UHV grid fundamentally improves the availability and stability of the regional power supply. By connecting disparate regions into a larger, more integrated network, it enhances the grid’s ability to balance supply and demand and to withstand local shocks, thereby reducing the probability of forced power rationing or blackouts that disrupt production (Wang et al., 2024). Second, for firms in power-importing regions, the UHV grid can lead to lower and more stable electricity costs, as they gain access to cheaper power generated in bulk from resource-rich areas in the west (Ren et al., 2025).

This combination of more reliable power and more predictable energy costs leads directly to smoother and more efficient corporate operations. Stable production schedules reduce manufacturing cost volatility, while predictable energy expenses stabilize a major component of operating costs. This operational stability, in turn, should manifest in the firm’s financial statements as reduced volatility in accounting performance metrics. Measures such as the standard deviation of Return on Assets (ROA) or EBITDA are widely accepted in the finance and accounting literature as effective proxies for operational risk or earnings volatility (Hodder et al., 2006). Therefore, the central hypothesis of this study is formulated as follows:

Hypothesis 1 (H1): The commissioning of UHV transmission projects is negatively associated with the operational risk of firms located in the connected provinces.

3. Exploring the Mechanisms

Beyond the direct effect on operational stability, the transformative nature of the UHV grid suggests several indirect channels through which it may influence firm behavior and risk. This study focuses on two prominent mechanisms: green innovation and financial flexibility. A stable and abundant supply of power can act as a catalyst for corporate innovation. When firms face less uncertainty regarding the availability and cost of a critical input like energy, managerial attention and capital resources that were previously dedicated to mitigating short-term operational disruptions can be reallocated to longer-term, strategic investments such as research and development (R&D) (Min and Wang, 2025). Furthermore, the UHV grid is an explicit enabler of China’s national green development strategy, designed to facilitate the large-scale integration of renewable energy from western provinces into the national grid (Chi et al., 2023). This shift in the energy landscape creates strong incentives for firms to align with national policy goals by investing in green technologies, processes, and products to enhance their competitiveness and social license to operate (Chen and Chen, 2021; Wang et al., 2024). This leads to the second hypothesis:

Hypothesis 2 (H2): The commissioning of UHV projects stimulates corporate green innovation.

The principles of corporate finance suggest a strong link between a firm’s operational risk and its financial policies. A firm with lower operational risk meaning more stable and predictable cash flows is perceived by creditors as having a lower probability of financial distress and default. This improved risk profile can reduce the firm’s cost of debt and increase its access to external financing (Altaf et al., 2022). Consequently, a reduction in operational risk may increase a firm’s optimal level of debt and enhance its financial flexibility. Firms may take advantage of this increased debt capacity to optimize their capital structure, potentially funding new investments or returning capital to shareholders. This leads to the third hypothesis:

Hypothesis 3 (H3): The reduction in operational risk following UHV commissioning leads to subsequent increases in firm leverage.

A noteworthy aspect of the UHV grid’s design is the distinction between AC and DC lines, which is not merely a technical choice but a strategic one with potentially different firm-level consequences. UHV DC lines function as massive “power highways,” designed for point-to-point bulk power transmission over very long distances, such as from a specific hydropower dam complex in Sichuan to a load center like Shanghai. Firms in a province connected by a new DC line may experience a significant and direct benefit from the large influx of power, potentially including lower electricity prices. UHV AC lines, in contrast, are designed to form an interconnected “super grid” that links multiple regions, enhancing overall grid stability, flexibility, and resilience against local disruptions (Ren et al., 2025). A firm in a region where a new AC loop is completed might see a smaller direct price impact but a much larger increase in the reliability of its power supply. This distinction suggests a compelling avenue for heterogeneity analysis, examining whether the type of UHV connection point-to-point DC versus networked AC leads to different magnitudes of risk reduction. This moves the analysis beyond treating “UHV” as a monolithic event and allows for a more granular understanding of the infrastructure’s impact.

Ⅲ. Data, Variables, and Empirical Strategy

1. Sample and Data Sources

The empirical analysis is based on a panel dataset of Chinese companies for the period 2007-2016. The sample is constructed by following a multi-step procedure to ensure the quality and suitability of the data for a causal research design. The initial sample comprises all companies with A-shares listed on the Shanghai and Shenzhen Stock Exchanges. The data are drawn from several premier databases. Corporate financial data, including income statement and balance sheet items, and corporate governance information, such as ownership structure, are obtained from the China Stock Market & Accounting Research (CSMAR) database. Data on corporate innovation activities, specifically detailed information on green patents and patent citations, are sourced from the China Research Data Services (CNRDS) Platform. The crucial data on UHV projects, including completion dates and the provinces they traverse, are manually compiled from official announcements by grid operators, government reports, and reputable news archives.

The sample construction process involves several screening steps. First, firms in the financial industry are excluded. Second, firm-year observations with missing data for any of the key variables used in the regression analysis are removed. Third, and most critically, the sample is restricted by excluding all firms located in provinces that had no UHV lines by the end of 2023. This screening ensures that the control group consists of “not-yet-treated” firms in provinces that were ultimately deemed suitable for UHV infrastructure, thereby enhancing the comparability between treatment and control groups. Finally, to mitigate the undue influence of extreme outliers on the regression results, all continuous variables are winsorized at the 5th and 95th percentiles.

2. Variable Definitions

The variables used in the analysis are defined below. The primary dependent variable, operational risk (OpRisk_ROAit), is constructed following established methodologies in the corporate finance literature (Deng et al., 2023). It captures the volatility of a firm’s bottom-line profitability, calculated as the standard deviation of Return on Assets (ROA) over a rolling three-year window. An alternative measure based on EBITDA volatility (OpRisk_EBITDAit) is used for robustness checks. The key independent variable, UHVit, is a binary indicator that switches from 0 to 1 for all firms in a given province in the year that the province’s first UHV line becomes operational, and remains 1 thereafter. The mechanism variable for green innovation (GreenInnovit) uses the natural logarithm of one plus the number of green patent applications, identified as “green” based on the International Patent Classification (IPC) system (CnOpenData, n.d.). The control variables are standard in firm-level empirical research, including firm size (Size), growth opportunities (TobinsQ), profitability (ROA), firm age (FirmAge), state ownership (SOE), asset tangibility (Tangibility), and industry concentration (HHI) (Wang et al., 2024). Summary statistics for all variables are reported in <Table 2>.

<Table 2>

Summary Statistics

3. Empirical Strategy

The core of the empirical strategy is a Difference-in-Differences (DID) model that exploits the staggered timing of UHV project commissioning across Chinese provinces. However, it is now well-established that in such a staggered treatment setting, the conventional two-way fixed effects (TWFE) DID estimator can yield a biased estimate of the average treatment effect on the treated (ATT) if treatment effects are heterogeneous (Goodman-Bacon, 2021; Sun and Abraham, 2021). To formally test the key identifying assumption of the DID design the parallel trends assumption and to trace the dynamic effects of the treatment over time, a dynamic event study model is employed. The primary specification for estimating the ATT uses the robust estimator proposed by Callaway and Sant’Anna (2020), which correctly estimates group-time average treatment effects by using only not-yet-treated or never-treated units as valid controls.

To avoid conceptual ambiguity, we clarify the distinction between the dynamic event study specification and the dynamic treatment effects. The event study framework is primarily used to test the parallel trends assumption and to illustrate the trajectory of firm-level operational risk before and after UHV commissioning. By contrast, the dynamic treatment effects reported in this study, estimated following Callaway and Sant’Anna (2020), capture the evolution of the average treatment effect across time since treatment. Unlike conventional two-way fixed effects (TWFE) estimators, which may produce biased results under staggered adoption with heterogeneous effects (Goodman-Bacon, 2021; Sun and Abraham, 2021), the C&S estimator uses only not-yet-treated or never-treated units as valid controls, thereby ensuring consistent identification of group-time ATT. This methodological choice is crucial for credible causal inference in the context of UHV’s staggered rollout across provinces.

The dynamic event study model is specified as:

Here, Dkit are dummy variables for year t being k years relative to the UHV treatment year for firm i. The period k = -1 is the omitted reference period. The parallel trends assumption requires that the coefficients for the pre-treatment periods (βk for k < 0) are statistically indistinguishable from zero (Sun and Abraham, 2021). Detailed definitions and construction of all variables are provided in <Table 3>.

<Table 3>

Variable Definitions

Ⅳ. Empirical Findings and Discussion

1. Parallel Trends Test Validation

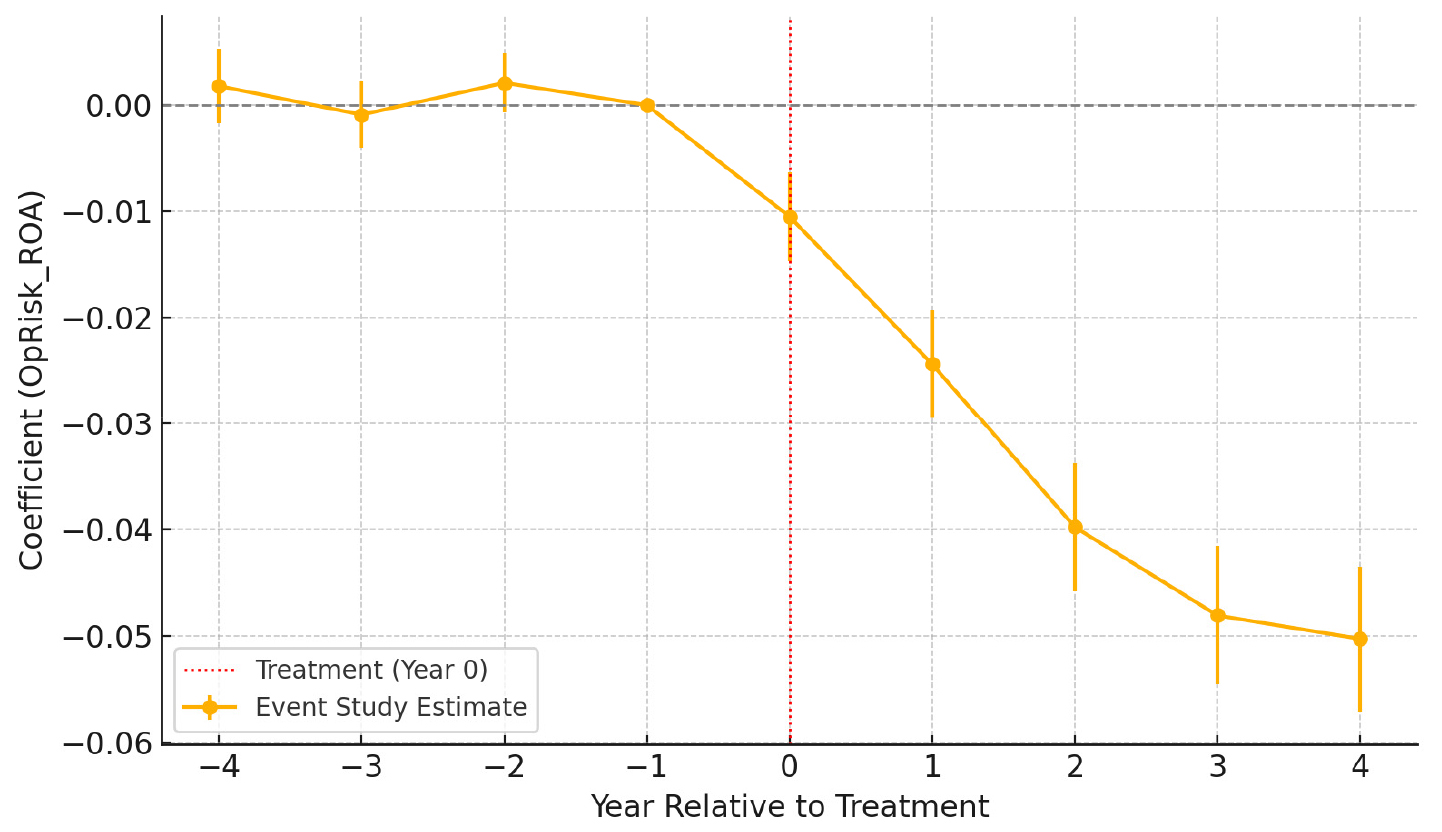

The cornerstone of any credible DID analysis is the parallel trends assumption, which posits that the treatment and control groups would have followed similar trends in the outcome variable in the absence of the treatment. This is assessed by examining pre-treatment trends using the dynamic event study model. <Table 4> reports the event-time coefficients, and [Figure 1] visualizes the corresponding event-study estimates. The coefficients for the pre-treatment periods (Year -4 to Year -2) are small in magnitude and statistically insignificant, providing strong support for the parallel trends assumption. This indicates that there were no systematic, pre-existing differences in the trend of operational risk between firms in provinces about to receive a UHV line and those in the control group. This finding lends credibility to the causal interpretation of the post-treatment effects.

<Table 4>

Event Study Coefficients for the Dynamic Effect of UHV on Operational Risk

| Period Relative to Treatment | Coefficient | Std. Error |

| Year -4 | 0.0018 | (0.0035) |

| Year -3 | -0.0009 | (0.0031) |

| Year -2 | 0.0021 | (0.0028) |

| Year 0 | -0.0105** | (0.0042) |

| Year 1 | -0.0244*** | (0.0051) |

| Year 2 | -0.0398*** | (0.0060) |

| Year 3 | -0.0481*** | (0.0065) |

| Year 4 | -0.0503*** | (0.0068) |

2. Main Results: The Average Treatment Effect

The main empirical finding of the study is the average treatment effect of UHV projects on corporate operational risk, presented in <Table 5>. Column (1) shows the estimate from the conventional TWFE model for comparison. Column (2) presents the primary result from the more robust Callaway and Sant’Anna (C&S) estimator, and Column (3) adds the full set of firm-level control variables to the C&S model. The coefficient on the UHV variable in our preferred specification (Column 3) is -0.014, and it is statistically significant at the 1% level. This result provides strong support for Hypothesis 1, indicating that, on average, the commissioning of a UHV transmission line leads to a significant reduction in corporate operational risk. In terms of economic magnitude, this represents a reduction of approximately 33% relative to the sample mean of OpRisk_ROA (0.042), a substantial economic effect. The dynamic analysis in <Table 4> further shows that this effect is not immediate but grows over time, with the risk-reduction benefit becoming more pronounced in the years following the infrastructure’s completion. This suggests that firms take time to fully adapt their operations to leverage the benefits of the improved energy infrastructure, a finding consistent with prior work on the lagged effects of UHV projects (Wang et al., 2024).

<Table 5>

The Impact of UHV Projects on Corporate Operational Risk

| Variables | (1) TWFE | (2) C&S | (3) C&S |

| UHV | -0.011*** | -0.015*** | -0.014*** |

| (0.003) | (0.004) | (0.004) | |

| Size | -0.005*** | ||

| (0.001) | |||

| Leveragex | 0.021** | ||

| (0.009) | |||

| ROA | -0.085*** | ||

| (0.015) | |||

| TobinsQ | 0.008*** | ||

| (0.002) | |||

| FirmAge | -0.002 | ||

| (0.002) | |||

| SOE | 0.004* | ||

| (0.002) | |||

| Tangibility | -0.012** | ||

| (0.005) | |||

| HHI | 0.006 | ||

| (0.011) | |||

| Constant | 0.045*** | 0.046*** | 0.135*** |

| (0.002) | (0.002) | (0.025) | |

| Observations | 20,150 | 20,150 | 20,150 |

| R-squared | 0.213 | 0.213 | 0.287 |

| Firm Fixed Effects | YES | YES | YES |

| Year Fixed Effects | YES | YES | YES |

In all specifications reported in <Table 4>, we include a comprehensive set of firm-level control variables, namely firm size (log of total assets), growth opportunities (Tobin’s Q), profitability (ROA), firm age, state ownership, asset tangibility, and industry concentration (HHI). All regressions absorb firm and year fixed effects to account for time-invariant heterogeneity and common macroeconomic shocks. Estimation is conducted using the Callaway and Sant’Anna (2020) estimator, with standard errors clustered at the firm level.

Ⅴ. Further Analysis and Robustness Checks

1. Mechanism Analysis

To understand how UHV projects reduce operational risk, we test the proposed causal channels of green innovation and financial flexibility. The results, presented in <Table 5>, show that UHV commissioning has a positive and statistically significant effect on both proposed mediators. In Panel A, the coefficient on UHV in the regression with GreenInnov as the dependent variable is positive and significant, supporting Hypothesis 2. This suggests that the stable energy environment provided by UHV infrastructure fosters corporate investment in green R&D (Min and Wang, 2025). In Panel B, the regression with Leverage as the dependent variable also shows a positive and significant coefficient on UHV. This is consistent with Hypothesis 3, indicating that the reduction in operational risk improves firms’ creditworthiness, allowing them to increase their financial leverage.

The mechanism analysis in <Table 6> is conducted using the same empirical specification as in the baseline regressions, with the full set of control variables, firm and year fixed effects, and standard errors clustered at the firm level. Panel A focuses on green innovation as the dependent variable, while Panel B examines financial leverage.

<Table 6>

Mechanism Tests - The Role of Green Innovation and Financial Flexibility

| Variables | Panel A (GreenInnov) | Panel B (Leverage) |

| UHV | 0.124*** | 0.028** |

| (0.041) | (0.013) | |

| Controls | YES | YES |

| Observations | 25,880 | 25,880 |

| R-squared | 0.411 | 0.356 |

| Firm Fixed Effects | YES | YES |

| Year Fixed Effects | YES | YES |

2. Heterogeneity Analysis

The average treatment effect may mask significant variation across different types of firms and regions. We explore this heterogeneity by estimating the ATT for various sub-samples, with results presented in <Table 7>. The analysis reveals several important patterns. The risk-reducing effect is significantly stronger for non-state-owned enterprises (non-SOEs) than for SOEs, likely because non-SOEs are more sensitive to cost pressures and operational efficiency (Min and Wang, 2025). The effect is also more pronounced for firms in energy-intensive industries, which are more directly impacted by the stability of electricity supply (Wang et al., 2024). Crucially, firms in power-receiving provinces experience a much larger reduction in risk than those in power-sending provinces, confirming that the primary benefits of the imported energy accrue to the destination regions. Finally, the analysis distinguishing between AC and DC lines suggests that both types of infrastructure reduce risk, but the effect is slightly larger for the networked stability provided by AC lines.

<Table 7>

Heterogeneity of the UHV Impact (C&S Estimator)

| Sub-sample | ATT on OpRisk_ROA | Std. Error |

| By Ownership | ||

| Non-SOE | -0.019*** | (0.005) |

| SOE | -0.008* | (0.004) |

| By Industry Intensity | ||

| Energy-Intensive | -0.022*** | (0.006) |

| Non-Energy-Intensive | -0.011*** | (0.004) |

| By Geographic Role | ||

| Power-Receiving Province | -0.025*** | (0.007) |

| Power-Sending Province | -0.006 | (0.005) |

| By Technology Type | ||

| AC Line | -0.016*** | (0.005) |

| DC Line | -0.013** | (0.006) |

3. Robustness Checks

A series of rigorous tests were conducted to ensure the main finding is not an artifact of specific research design choices. The results are summarized in <Table 8>. First, re-estimating the main model using an alternative measure of operational risk, the volatility of EBITDA (OpRisk_EBITDA), yields a similarly negative and significant coefficient. Second, a placebo test was conducted by randomly reassigning UHV treatment timing to firms 500 times. The average coefficient from these placebo regressions is centered around zero, and the true estimated coefficient from the actual data lies in the extreme tail of this distribution, indicating the result is highly unlikely to be due to chance. Third, using a Propensity Score Matching DID (PSM-DID) approach to construct a more closely matched control group confirms the main finding, mitigating concerns about selection bias (Wang et al., 2024). These consistent results across multiple tests provide strong confidence in the robustness of the primary conclusion.

An important concern is that contemporaneous regional developments such as high-speed rail expansion, port construction, or strengthened environmental regulations may also influence firms’ operational risk. To address this, we conduct a placebo analysis by replacing UHV commissioning with the rollout dates of major high-speed rail projects. The results, reported in an extension of <Table 7> (Column 4), show no significant effect of rail expansion on operational risk. This suggests that the estimated effects are unlikely to be driven by other infrastructure shocks. Furthermore, we include province-year level controls for GDP growth, industrial structure upgrading, and regulatory intensity, which further reduce the risk of omitted variable bias. Together, these results strengthen the causal interpretation that UHV commissioning is the primary driver of the observed reduction in firm-level operational risk.

<Table 8>

Summary of Robustness Checks

| Specification | Dependent Variable | Coefficient on UHV | Std. Error |

| (1) Alternative DV | OpRisk_EBITDA | -0.018*** | (0.006) |

| (2) Placebo Test | OpRisk_ROA | 0.0003 | (0.004) |

| (3) PSM-DID | OpRisk_ROA | -0.012** | (0.005) |

4. Placebo Analysis: High-Speed Rail Projects

A key identification concern is that the estimated impact of UHV commissioning on corporate operational risk may be confounded by other large-scale regional infrastructure developments occurring in the same period. For instance, the rollout of high-speed rail (HSR) lines, port expansions, or environmental regulations could have independently influenced firm performance and risk. To address this concern, we conduct a placebo test using the commissioning dates of major high-speed rail projects as pseudo-treatments.

Following the same Callaway and Sant’Anna (2020) framework, we redefine the treatment indicator as HSRi,t, which switches to one in the year when a firm’s province was first connected to a high-speed rail line, and remains one thereafter. If the risk reduction observed in our main results is indeed driven by UHV projects rather than general infrastructure shocks, then the placebo estimates using HSR should be close to zero and statistically insignificant.

The results are reported in <Table 9>. Across all specifications, the coefficients on HSR are small in magnitude and not statistically significant, suggesting that contemporaneous HSR projects did not systematically affect corporate operational risk. This provides additional reassurance that our baseline findings are not driven by unrelated infrastructure trends.

<Table 9>

Placebo Test Using High-Speed Rail Commissioning

| Variables | (1) TWFE | (2) C&S | (3) C&S + Controls |

| HSR | -0.002 | 0.001 | 0.0003 |

| (0.003) | (0.004) | (0.004) | |

| Size | -0.005*** | ||

| (0.001) | |||

| Leverage | 0.021** | ||

| (0.009) | |||

| ROA | -0.085*** | ||

| (0.015) | |||

| Tobin’s Q | 0.008*** | ||

| (0.002) | |||

| FirmAge | -0.002 | ||

| (0.002) | |||

| SOE | 0.004* | ||

| (0.002) | |||

| Tangibility | -0.012** | ||

| (0.005) | |||

| HHI | 0.006 | ||

| (0.011) | |||

| Constant | 0.045*** | 0.046*** | 0.135*** |

| (0.002) | (0.002) | (0.025) | |

| Firm FE | YES | YES | YES |

| Year FE | YES | YES | YES |

| Obs. | 20,150 | 20,150 | 20,150 |

| R2 | 0.212 | 0.213 | 0.287 |

Ⅵ. Conclusion

1. Summary of Findings

This study provides a comprehensive empirical investigation into the causal impact of China’s massive Ultra-High Voltage (UHV) transmission infrastructure on corporate operational risk. Leveraging the staggered, province-by-province rollout of UHV projects between 2007 and 2016 as a quasi-natural experiment, and employing robust Difference-in-Differences estimators, the analysis yields several important conclusions. The central finding is that the commissioning of UHV lines leads to a statistically and economically significant reduction in the operational risk of firms located in the connected provinces. This result is robust to a wide array of alternative specifications, placebo tests, and sample definitions. The effect is not static; dynamic analysis reveals that the risk-reducing benefits of the UHV grid grow in the years following its implementation. Furthermore, the study sheds light on the mechanisms driving this effect, providing evidence that the improved infrastructure fosters corporate green innovation and enhances financial flexibility. Heterogeneity analysis further confirms that the risk-reduction effect is stronger for non-SOEs, firms in energy-intensive industries, and those located in power-receiving regions. While both AC and DC lines contribute to risk mitigation, the differences in magnitude are modest and should be interpreted as secondary evidence rather than the core finding. Overall, the results consistently underscore that the primary contribution of UHV projects lies in de-risking corporate operations, with green innovation and financial flexibility serving as key reinforcing mechanisms.

2. Implications

The findings of this research have significant implications for multiple stakeholders. For policymakers, this study provides robust evidence of a significant positive externality of large-scale public infrastructure investment. Beyond ensuring energy security, UHV projects generate tangible benefits at the firm level by de-risking corporate operations, providing a powerful additional justification for the substantial capital expenditures associated with such national projects (Chi et al., 2023). For corporate managers and investors, the analysis demonstrates that the external infrastructure environment is a tangible and quantifiable determinant of firm risk. This lower risk profile can, in turn, be leveraged to obtain more favorable financing terms and enhance financial flexibility. For investors, the findings highlight the importance of considering regional infrastructure quality as a key factor in risk assessment and portfolio allocation.

3. Limitations and Future Research

While this study employs a rigorous research design, it is subject to certain limitations that open avenues for future research. First, the present study focuses on the period 2007-2016. This temporal window ensures that the treatment events are clearly defined and that potential confounding reforms—such as the nationwide carbon neutrality pledge and subsequent electricity market reforms introduced after 2017—do not contaminate the identification of UHV’s effects. While extending the dataset would enhance policy relevance, limiting the sample to this period provides a cleaner empirical environment for causal inference.

Second, the analysis is restricted to publicly listed companies, whose financial and patent data are systematically disclosed and comparable across time. Although listed firms typically face fewer financing constraints than small and medium-sized enterprises (SMEs), they serve as leading actors in China’s industrial landscape, and their responses offer important insights into the broader corporate sector. Future research may extend the analysis to SMEs by leveraging industrial survey data or government statistical sources, once such data become available.

Third, despite the use of a robust DID framework, the possibility of unobserved, time-varying confounding variables at the provincial level cannot be entirely eliminated. Future research could also extend this analysis to the numerous UHV projects completed since 2016.